#14 - Finance Fridays - Bottom Up Strategy, Ray Dalio’s Investing Advice, British ISA Candidates

This is the Reality Cheque’s newsletter where I document my journey to financial freedom through learning more about personal finance. Every week expect curated content on personal finance, career advice and entrepreneurship. And the best part is it'll always be less than 5 minutes to read!*This is not financial advice, just me brainstorming about things related to money. Stocks are extremely volatile - value can go down as well as up. All investments and income streams may be subject to tax.

Contents:

💡 Idea of the Week - Taking the Ray Dalio’s Approach for the British ISA

🥗Side Hustle of the Week - UK Treasury Bills

🎒Useful Resource - S&P 500 Might Not Return 10%

🎒Useful Resource - Saving Money With Friends

💹 Investing - Investing Strategy for Dummies - Bottom Up vs Top Down

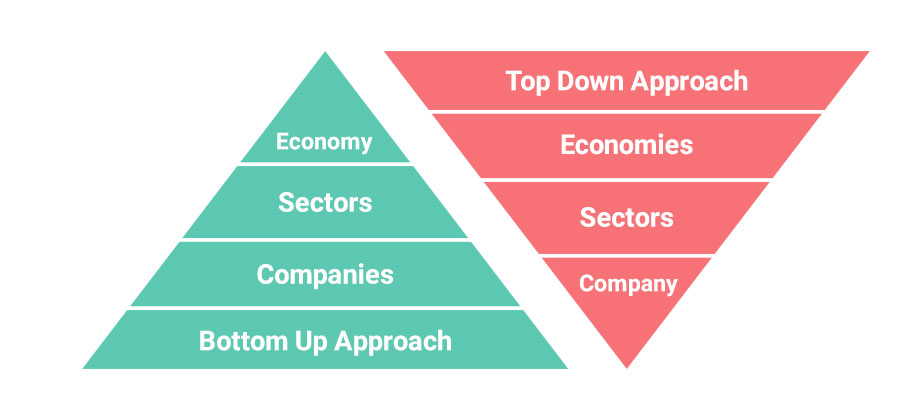

💹 Investing Strategy for Dummies - Bottom Up vs Top Down

Inspired by How To Pick And Analyze Stocks (Complete Guide)

This YouTube video was a great overview of how to start picking stocks and the part I wanted to highlight was the Top-Down vs. Bottom-Up Strategy section.

The difference is the bottom-up investors focus on a specific company and its fundamentals, whereas top-down investors focus on the industry and economy.

The Bottom-Up Strategy would be me:

1. Picking a stock I like

2. Reviewing the Industry and the main competitors in it

3. Reviewing the Market/Economy it is in

4. Reviewing the Global Trends that may work in favour or against the company’s business model

The Top-Down Strategy would be me:

1. Looking at the Global Economy

2. Narrowing my search down to countries I understand (home sweet home)

3. Picking a few key industries (and specialising in those)

4. Analysing the top companies in each industry

5. Choosing the best candidates for future growth

For amateur investors, I believe we should focus on what we intuitively understand. Companies you regularly interact with would fit this description meaning I would probably favour the bottom up strategy.

For example, I understand football even though I don't read the annual statements of football clubs. A hedge fund manager or a stock broker will have me beat on reading into any company’s financials including football clubs. But I would have a better read on whether Chelsea spending 1 billion on a team of unproven talent would ever turn into a good investment. An American accountant who thinks football means NFL, would probably view Boehly’s investment strategy as a long term view rather than outright recklessness.

Everything has been priced in (in the words of /r/wallstreetbets) so I just prefer to focus on the intangibles that will materialise long term. This reminds me of a YouTuber making money on the stock market because he saw a TiKTok trend. I'm not saying invest based on TikTok trends but intuition to me seems like a better way to “beat the market” than pouring over the same financials everyone else is looking at.

💡 Taking the Ray Dalio’s Approach for the British ISA

Ray Dalio’s Holy Grail strategy is that if you have 15 or more good, uncorrelated return streams, you will reduce your risk by about 80%. I went down a rabbit hole and realised in spite of his fame, he might have been more wrong than right in the last decade but the logic is pretty sound.

So how do you pick 15 uncorrelated return streams?

1. Find different industries/sectors I like

The GICS structure consists of 11 sectors, 25 industry groups, 74 industries and 163 sub-industries. Industries are too broad in definition so I would like to narrow down to specific sectors. For example, “Food, Beverage and Tobacco” are one Industry Group but in reality are not correlated. As a consumer, I will always need food which is sometimes accompanied by a beverage (not tap water). Then there’s tobacco which is a hobby in its own category. These are different propositions entirely.

2. Focus on the nuances of customer personas

The purchasing habits of active lifestyle city dwellers are probably uncorrelated with Gen Z university students outside the country’s capital. There are many ways to slice these personas, filtering based on demographics, racial background, generations and more.

3. Be specific on the products/services you want to invest in

The sales of avocado and barista coffee wouldn’t be correlated to PC Graphic Cards (unless there’s a MacBook involved - IYKYK). And then if you break down each product category by price point (low, medium, high), you would see different economic trajectories for each group. For example, how correlated are the fortunes of fine dining restaurants with McDonald’s franchisees? Not at all.

If you keep niching down sectors, consumers and products that interest you, you’ll eventually reach 15 companies you understand well enough.

How would you apply this?

One criticism is, are we spreading ourselves too thin choosing 15 individual stocks? Like mentioned in another section of this newsletter, developing a specialty in multiple industries would be very hard. Especially if it isn’t your full time job.

But if we focused on one market, you would at least know the products and services you use everyday well enough without needing to have a specialist understanding of each sector.

This strategy would probably fit the British ISA since there’s only so many companies one can invest in the UK that’s actually worth your time - given the state of the UK economy long term. But there will be companies that will perform well even in bad economic conditions due to brand affinity and price elasticity of their products.

15 UK Companies to Put In your British ISA by Compounding Investor.

Hikma Pharmaceuticals

United Utilities Group

Severn Trent

National Grid

RS Group PLC

DRAX Group PLC

Smurfit Kappa

Intermediate Capital Group PLC

SEGRO PLC

Safestore Holdings PLC

Sirius Real Estate

Fidelity Special Values

Mercantile Investment Trust

3i Infrastructure PLC

Law Debenture Corporation PLC

Maybe I’ll try it when the British ISA goes live but I would rather max out my current ISA first without the British restriction.

🎒 S&P 500 Might Not Return 10%

Inspired by - Do Stocks Return 10% on Average?

The main takeaways from this video are that US stock valuations are historically high which means lower returns in the future. And if we’re being fair, it has returned closer to 7% not 10% in real returns. Others claim that the actual average return -- after adjusting for inflation, reinvesting dividends, and assuming you pay no taxes-- is almost half that.

This is still better than other forms of investments but if you have a specific number in mind for retirement, you might want to temper your expectations.

S&P 500 is still a good return but it might be exaggerated due to a simple average return calculation. Here’s an example of how simple average returns can be misleading:

Invest £100 into Company A

Account in Year 1 = £200 (+100% return)

Account in Year 2 = £100 (-50% return)

Simple Average Return = +75% but you have gained nothing.

Still stocks will probably keep going up in the super long term which is better than cash sitting in your bank account.

🎒Saving Money With Friends

If you ever wanted to save money with friends, have you heard of Bloom?

“It involves an informal gathering of people from a certain community who act as a bank, collecting and saving money that members can withdraw. A way to conduct financial matters with people you trust.” - TechCrunch

This feels like an extension of Monzo’s Shared Pots feature or PayPal’s discontinued Money Pool but without the ability to actually pay for things as a group thus it’s still quite limited.

With the cost of living being a frequent topic of conversation, people have talked about raising capital within friendship groups. Unfortunately, companies are not incentivised to provide such services. In my opinion this is because investment groups amongst friends offer all the advantages banks want to offer at a price. Trust, security, credit. Banks would rather do that and take a cut in the form of fees.

Unfortunately this Bloom app is not filling the void of groups working together to invest in actual assets and financial freedom. And it is not FSCS protected at the time of writing.ctionable Advice

🥗Side Hustle of the Week 🚥 (UK Treasury Bills)

Inspired by How To Buy UK Government Bonds (Gilts)

The UK Government has now made UK Treasury bills available to everyday consumers with a typical 28-day maturity. Every Friday, the UK Debt Management Office (DMO) issues new UK Treasury bills through tenders. For example, these are how the numbers work out:

Initial investment: £1,000

Annualised yield: 5%*

Period yield: £1,000 5% 28 / 365 = £3.84

Total amount after one 28-day period: £1,000 + £3.84 = £1,003.84

When your UK Treasury bill matures, you will receive the amount you invested plus the yield, as cash. If you do this through the FreeTrade platform, it’s reinvested immediately.

The above calculations do not take into account any fees.

Previously, if you wanted to participate in the weekly tender process, you needed to have at least £500,000 and an account with a primary participant. Now you only need 50 quid.

🔴 - Potential dealbreaker

🟡 - It depends

🟢 - Very Ideal

1. Hours per week 🟢 - Borrowing money takes a couple of minutes, can’t complain

2. Skill required 🟢 - Freetrade will handle all the logistics

3. Up front cost 🟢 - You can borrow little as £50 but you wouldn’t get much back if you did that.

4. Market saturation 🟢 - Not a factor in this scenario

5. Timeline to reach success 🔴 - You wouldn’t really succeed at this

6. Income potential 🔴- No more than a savings account

In summary, it’s a randomised savings account that accumulates every 28 days. Looking at the Weekly Reports, you’re getting 5%-ish in a calendar year which is the same as a lot of current Savings Accounts and ISAs (which are tax free). I’m not too impressed but it’s an option.

✍🏿Quote of the Week

“You should find a couple of industries and become an expert in those industries. Don’t try be a Jack of All Trades for all the sectors in the market or you’ll end up being mediocre at that”