#13 - Finance Fridays - UK Home Ownership Schemes, Negative Equity, Side Hustling as an Online Coach

This is the Reality Cheque’s newsletter where I document my journey to financial freedom through learning more about personal finance. Every week expect curated content on personal finance, career advice and entrepreneurship. And the best part is it'll always be less than 5 minutes to read!Disclaimer: This is not financial advice, I’m just brainstorming ideas related to money.

Contents:

🧐 Question of the Week - Are Home Ownership Schemes like Help to Buy a scam?

🤔 Dilemma of the Week - When You Can’t Move Out of Your Flat

✅ Actionable Advice - 10 Questions to ask When Applying for Save to Buy

🥗Side Hustle of the Week - Online Coaching

💹Investment Idea review - Property

🧐 Are Home Ownership Schemes like Help to Buy and 99% Mortgages a scam?

UK Housing is a bit bonkers right now (like the rest of the western world). And between the government's obsession with propping up the housing market and house buyers needing every edge they can get, housing schemes are pretty popular.

But have they been a net positive for homeownership in the UK or have they screwed us over in the long term? For first-time buyers, I would say it has made things worse for 3 reasons:

Drove demand for leasehold flats which charge ludicrous additional charges like ground rent and service charges.

For example, Lewis Ryan, who owns 60% of a flat in Dalston, east London says his monthly service charge went from an initial £94 a month to £515 by April 2023 to £646 in 2024.

Inflated housing prices further down the line at an unsustainable rate.

10 years on, The Guardian has written about how private developers have been using the scheme to inflate the price of new flats, effectively pocketing the state subsidy of the Help to Buy and Share Ownership schemes for themselves.

Trapped first-time buyers into flats they can no longer afford to leave.

Most first home purchases are not forever homes. Research shows that 60% of first-time buyers (FTBs) live in their first property for less than five years with 20% moving within 2 years. This recent period of low interest rates has brewed this theory that we should get on the property ladder at any cost, even if you only intend to live there for a couple years.

People were so confident in this idea, they took out interest-only mortgages hoping the future equity would offset whatever rates they will be paying in an unknown future.

And it worked for many. I'm even envious that I didn’t take advantage of the lucrative housing market 5-10 years ago. But it has led to a new growing phenomenon called - negative equity.

🤔 Negative Equity - When you can't move out your flat

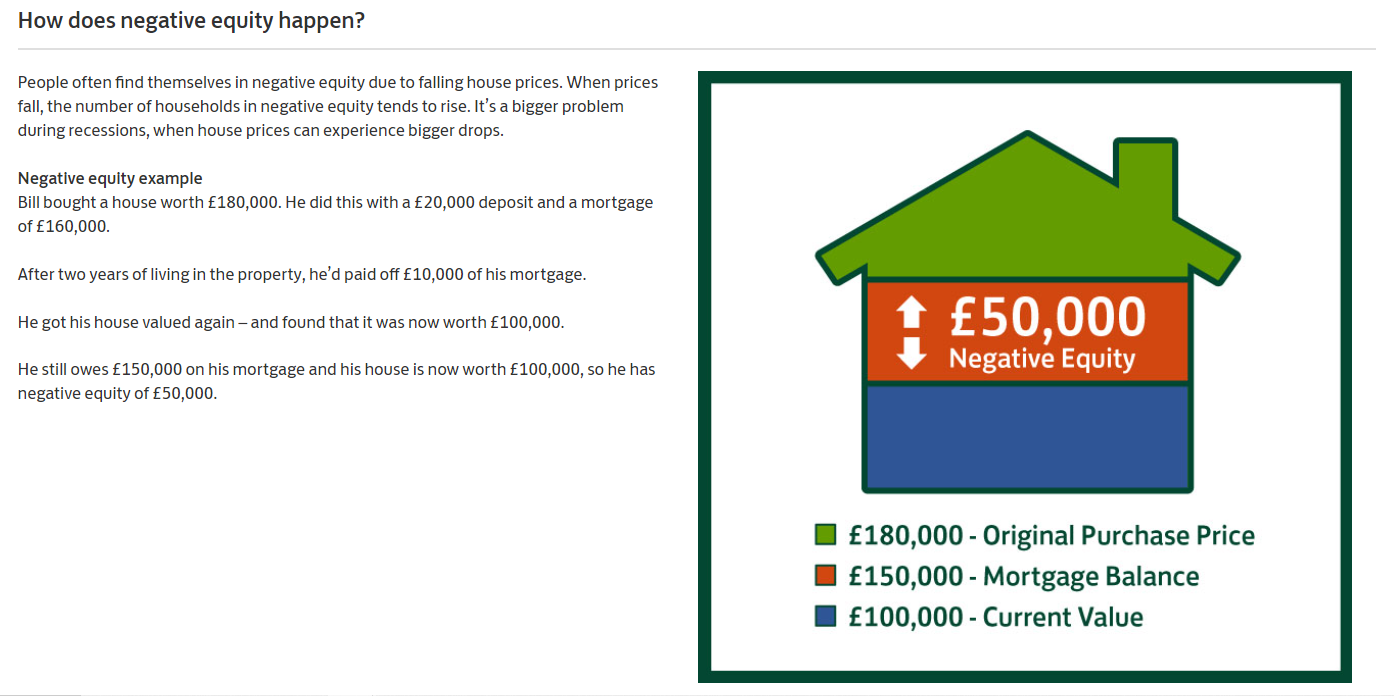

“Negative equity is when your property becomes worth less than the remaining value of your mortgage. To be in negative equity, the value of your house must fall below the amount you still owe on your mortgage”. - Lloyds Bank

In the long term, house prices always go up because land is finite and people will always need shelter. But a poorly built box stacked amongst other boxes, with additional charges every month can actually decrease in value in the short term.

And first-time buying flat owners are most likely there for the short term.

You can't remortgage if you're in negative equity because the lender would have to provide you a loan that exceeds the price of your house (loan-to-value over 100%). And if they do, it probably means you need to repay that remaining amount separately, damaging your credit score, jeopardising future mortgage deals. This 💩 could spiral.

New builds are usually more expensive against similar properties available in the secondary market. Therefore, a small house price dip in the market will hit your expensive, new build flat a lot more. So your plan to sell your flat in the next 5 years to move into your forever home has now backfired.

In summary, this is how Help to Buy (now expired) and Share Ownership schemes could have screwed many people over:

Your new build flat is already overvalued vs. the rest of the market

You are paying back the mortgage and maybe the Government scheme loan once the grace period expires (2-5 years for HTB)

The service charge and ground rent keep going up every year

The standard variable rate in the high interest environment is more expensive than ever before

The wider economic environment has caused house prices to stop increasing because the government’s short term policies have come home to roost.

And guess what the solution for all this is?

So what can we learn from all this as first time buyers?

✅ 10 Questions Before Using the next UK Housing Scheme

Property will always be a great investment but please, don’t be like Lewis, Michael or this couple and join a Home Ownership Scheme that’s too good to be true without knowing what you’re getting into.

I recently wrote down these questions before attending a viewing for a housing development for the Save to Buy scheme. Feel free to borrow them at your next viewing.

1. What is the minimal and maximal deposit I can pay?

The catch with low deposits is higher monthly charges. These schemes all offer low deposits so there’s more equity left over to charge against in the future. The bigger the loan(s), the bigger interest payment 💳 . Some would say it’s exploitation 🤷

2. Under what circumstances will the monthly payments increase?

It is extremely likely that the mortgage will be subject to change (hey Bank of England!). Knowing what circumstances will cause your bill to increase is vital.

3. What is the fixed/standard variable interest rate?

The interest rate will have a big impact on your monthly payments so try identifying any points of negotiation to keep rates within a manageable range. For example, what can you do to lock in a longer fixed rate?

4. Which lenders have accepted this scheme?

Not every bank is going to accept every Housing Scheme the UK government cooks up. Thus knowing which banks you can go to to secure the mortgage is pretty important.

5. Under what circumstance would I get initially rejected from this Scheme?

A lot of schemes are promoted as a way to get first time buyers on board but from what I've seen, they are just as inaccessible. For example, the Save to Buy viewing I went to, needed someone on a minimum annual salary of £70k.

Now can someone explain to me how the bank deems someone who is incapable of saving a 5% deposit, but can somehow afford total monthly payments of £1800 (when you add up all the charges)?

6. What is the average value of flats in the area?

As discussed in a previous section, new builds charge a premium price. That premium can bite you in the 🍑 if you ever wanted to sell or remortgage in a housing decline.

7. Which companies were involved in the development of this property?

Research their previous projects and developments to see if they can be trusted. 1 out of 3 people in a survey said that new build housing is 'poor-quality'. And for good reason, it got so bad that the government has made it so that leaseholders in private buildings would not be liable for the cost of remediating cladding defects found post purchase.

8. What are the other hidden costs?

9. Can I have pets?

Leasehold flats can have in place the most ridiculous rules (covenants) so ask for every restriction in writing before finding out your new home isn’t so homely.

10. When I sell or remortgage this place, what restrictions should I be aware of?

We’ve spoken about how negative equity can restrict your ability to remortgage your place. But it might not end there. Certain schemes have clauses in the fine print that ensure they extract as much money from you which usually means extortionate penalties for leaving early or keeping you on the lease for as long as possible.

💹Investment Idea review 🚥 (Property)

🔴 - Potential dealbreaker

🟡 - It depends

🟢 - Very Ideal

1. Potential upside 🟢 - It’s been one of the best forms of investments since capitalism

2. Level of risk 🟡 - The risk lies with the mortgage loan becoming too expensive as the recent interest rate hikes has shown

3. Upfront costs 🔴 - House deposits are one of the biggest barriers to most people ever getting on the property ladder

4. Historic performance 🟢 - House prices have risen so quickly that they have outpaced salaries by magnitudes

5. Skill required 🟢 - As long as you’re financially literate and have attention to detail you can purchase a house. The dumbest people I know have houses, since all the middlemen do all the leg work.

6. Market saturation 🟢 - The market is saturated from a buyer’s perspective and has been for a long time. This works in your favour as a homeowner whether you decide to rent it or sell it.

The obsession with getting on the property ladder is justified. The housing market defies the economic laws of supply and demand and has become so popular that it has distorted the very fabric of our western economies.

If you can afford it, get on it but as I’ve written through this newsletter there are many traps you can fall for if you’re not vigilant.

🥗Side Hustle of the Week 🚥 (Online Coaching)

🔴 - Potential dealbreaker

🟡 - It depends

🟢 - Very Ideal

1. Hours per week 🟡 - Depending on the coaching programme, you can land some great rates but the amount you can charge will be standardised alongside fellow coaches.

2. Skill required 🔴 - You’ll have be a natural at being good with people. You can definitely learn the soft skills to be a good online coach but to make good money requires an innate level of charisma and a friendly face

3. Up front cost 🟡 - Like most online jobs, there’s minimal joining costs but you will need to be qualified or at least complete some kind of course to be trusted enough to start coaching on the best platforms.

4. Market saturation 🟡 - The market isn’t saturated but there’s still a stigma around online coaching. You’ll be a small fish in a big pool starting out.

5. Timeline to reach success 🟡 - That’ll be down to the algorithm of the platform but the only thing working in your favour is that you don’t need a lot of customers to be successful since most of your clientele will be returning customers.

6. Income potential 🔴 - You’re still trading your time for money in a linear fashion removing potential for exponential growth and limits your earning potential to your free time.

✍🏿Quote of the Week

“The stock price changed but did physics change? Did gravity change? Did all the things we assumed that we believed that led to our decision, did any of that change?”