#21 - Finance Fridays - 100k Net Worth, Shared Ownership and Productivity Through Sacrifices

This is the Reality Cheque’s newsletter where I document my journey to financial freedom through learning more about personal finance. Every week expect curated content on personal finance, career advice and entrepreneurship. And the best part is it'll always be less than 5 minutes to read!*This is not financial advice, just me brainstorming about things related to money. Stocks are extremely volatile - value can go down as well as up. All investments and income streams may be subject to tax.

Contents:

🤔 Question of the Week - What do your Spending Habits say about you?

💸 Entrepreneurship - The most honest advice on building a side hustle

🏡 Housing - Should You Save Your Money or Do Shared Ownership?

💹 Investing - Why 99% of Financial Advice is not relevant to you

💹Why 99% of Financial Advice is not relevant to you

I've been looking for a way to conceptualise how applying financial advice changes every time you hit certain financial milestones. I think I’m going to call it - Purchasing Power Tiers.

Purchasing Power Tiers relates to how each financial milestone unlocks a category of opportunities to acquire new wealth. This concept just happens to be well articulated in this YCombinator Post on Bill Gates losing billions diversifying his Microsoft wealth based on Warren Buffet’s advice. These 3 comments offer different perspectives when it comes to accumulating different levels of wealth.

Comment 1:

With $138B you can eradicate a few diseases and give scholarships to all high performing poor children in the world for a decade.

With $1.33T you can do something like transform Colombia into a developed country.

Comment 2:

"What is true is that at this scale the incremental value of money is vastly diminished. Having an extra $10 makes an enormous difference if you have $4, it still makes a little difference if you have $400, it makes almost no difference at all if you have $138B."

Comment 3:

I think purchasing power isn't incremental when it comes to investing like people say it is. Start investing $5 isn't the same as $50.

Why is this important?

There’s a lot of financial advice that’s simply not appropriate based on your Purchasing Power Tier. For example, I find headlines like “Invest like the 1%” quite misleading. For a few reasons:

Reason 1: Compound Interest only really works it magic once you hit a certain threshold

Search 100k net worth on YouTube

There’s a reason why you see Youtube videos called “Why Your Net Worth Explodes at 100k”. It’s because investing up to that 100k point will only give you marginal gains and it is beyond that point that your decades worth of investment pays off.

Reaching £100,000 in net worth is like reaching 51 Poise in Elden Ring, until you reach that milestone all your effort prior is borderline meaningless. And why am I using a video game reference? Because the Elden Ring DLC is releasing next week at the time of writing.

Reason 2: Your strategy before the milestone is different after the milestone

For example let’s consider this financial milestones,

£30,000 - When you reach 3-6 months worth of living expenses/monthly salary - You can now consider taking a career risk which may or may not pay off in the long term. Such as transitioning to a new industry/role or turning your side hustle into a full-time business if there’s enough traction.

£100,000 - You have enough capital to set up your retirement pathway through big ticket investments like property. You may want to take less risks and focus on reliable compounding returns.

£500,000 - £1m - You can now make multiple high ticket, high risk investments that have the potential for exponential gains. This is how venture capitalists approach investing in start-ups. They only need one investment to make back the money they’ve invested. Or you can sweat the small stuff like fund fees and interest rates since 1% of £1 million is still £10,000 which is still significant even to you as a millionaire.

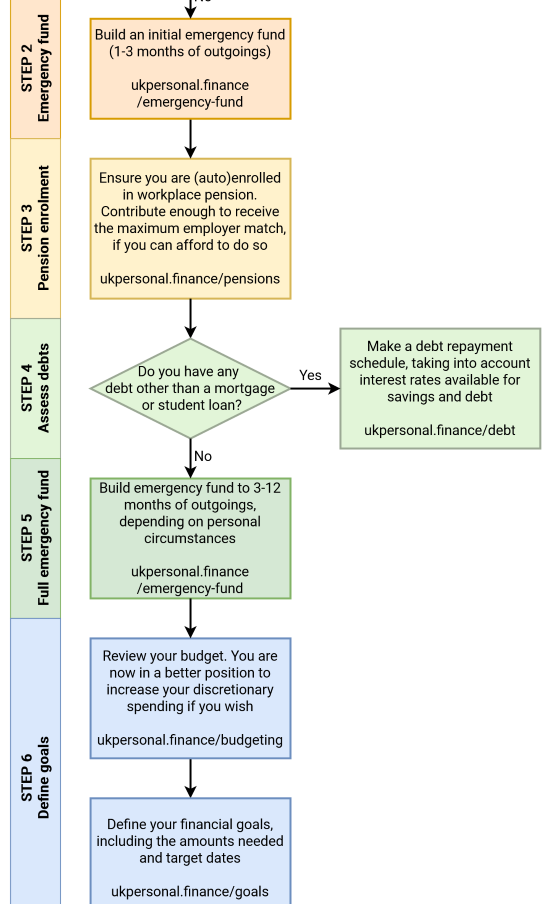

If that doesn’t make much sense, simply look at UKPersonalFinance’s Flowchart, it’s a very simpler concept but separated into Steps.

What level are you at based on these questions?

Flowchart by UK Personal Finance Subreddit

Takeaway 1 - I won’t be investing like the 1%

To me it doesn’t make sense to treat my £10,000, the way a rich person treats their £1,000,000 because they are 10% of our total net worth. They are two totally different tools for building wealth and the strategy a super rich person is using now probably isn’t the one they used when they were at my level.

Takeaway 2 - If I can’t reach £100k in net worth with 10-20 years left to compound, I need to re-evaluate.

I don’t personally see any value in a long term investing strategy that doesn’t hit the 100k mark with a few decades to go. That means if I was to be in such a position, taking more risks so I have more capital to invest would be better than investing every penny for a lifetime of incremental gains.

🏡Should You Save Your Money or Do Shared Ownership?

I saw this on Reddit and these are the calculations I would make. But firstly my assumptions:

Assumptions

Shared Ownership will be more expensive because it’s most likely a leasehold and you have to pay the mortgage and ground rent

There’s approximately a 5% return on average investing and on house prices

Shared Ownership is a short term venture to get on the property ladder and most will want to move out to secure their forever home

You would purchase around 25% of the property worth £400,000

You wouldn’t want to invest in a Stocks and Shares ISA with a 5 year time horizon due to volatility.

Costs | Shared Ownership (25% Of £400,000) | Renting |

Accommodation Costs | Rent + mortgage + Service charge (£2000) | Rent (£1000) |

Additional expenses | legal fees + stamp duty (£5000) | (£0) |

Lump sum spend | Deposit (£20000) | Cash ISA (£20,000) |

Investments | All spent on house (£0) | £1000 monthly (£60,000) |

Realised Gains After 5 Years (5%) | (£0) | (£13,673) |

Unrealised Gains After 5 Years (5%) | (£28,336) | (£0) |

Key takeaways:

WHEN you sell, would seem the biggest factor to me. Your capital gains on a property will always outstrip your investments. But given how difficult it can be to sell, you may not be able to control when you cash out.

Monthly Costs should be easily affordable in case future costs (leaseholder/interest rates) spiral out of control.

Are you able to increase your salary in 5 years to the point a house is now affordable or meet your future someone to go 50/50 with? There’s a huge opportunity cost if you over invest into a Shared Owned property.

In a low interest environment, investing in stocks would have been more appealing even with its volatility.

💸The most honest advice on building a side hustle

I’m a mom with a fulltime job. And I spent the last year writing a whole @** book. 📕 Here’s how I did it:

Normally LinkedIn Posts are very cringe but I like this one for one reason.

She said up front what she sacrificed.

Productivity is as much about making sacrifices as about gaining things.

Her health, home maintenance and social life suffered but it was the trade off she was willing to give in return for the dream of being an author.

What are you willing to sacrifice for your dream?

🤔 What do your Spending Habits say about you?

If you're the type that has struggled with saving money - have you thought about the motivations behind your spending habits?

These 3 questions are an exercise in doing just that.

1. Do you spend more than what you’ll like on designer clothes/partying?

2. Has FOMO (Fear of MIssing Out) made you make poor financial decisions?

3. Do you possess more items like clothing than you would ever need?

If you answered yes to more than two of those questions, then you're more likely to be influenced by external factors like peer pressure.

Consider what motivates you internally the things in life and spend in accordance to that. I feel you’re more likely to be happier in the long term with this approach.

✍🏿Quote of the Week

“You don't have to get to 100% certainty on decisions, get to 51%, and when you get there, make the decision and be at peace with the fact that you made the decision based on the information you had ”